Recovery from the LA fires is harder for homeowners who have lost insurance

Home insurance companies are increasingly refusing to protect vulnerable areas, as severe weather events become more common due to climate change

In the early hours last Wednesday, William Chandler attempted to save his home in Altadena, in Los Angeles County, choosing to stay behind after his wife and daughter safely evacuated. Donning a gas mask and fire resistant jacket—items long ago left behind by his father who worked as a city electrical engineer—Chandler had three hoses spraying water on the home, hoping to offer at least some protection from the fast-approaching fires, which finally hit his street around 4 a.m.

“My backyard was starting to catch fire, and the smoke just became unbearable, to the point where I was starting to get dizzy,” Chandler said in an interview. “That’s when I knew, OK, it’s time to go.”

Making that decision wasn’t easy. Chandler’s house was more than a home for his young family; it was also an heirloom passed down in his family for three generations.

“I grew up in that home. My dad grew up in that home,” Chandler said. “I think about the type of men that they were, and they wouldn’t run away from a fire to protect what was theirs.”

The home, which Chandler formally inherited in July after his grandfather’s death, burned down. In a crushing twist, the house had only recently become uninsured; Chandler had struggled to manage payments for the existing policy while juggling his grandfather’s nursing expenses, and his attempts to negotiate a more affordable payment structure failed. When Chandler tried to shop around for other insurance plans, he was routinely denied.

Losing his grandfather’s “pride and joy” is devastating, Chandler said, but “the fact that I don’t know if I could come back from it is by far the worst.”

As severe weather events such as the Los Angeles-area wildfires become more frequent due to climate change, insurance companies increasingly refuse to protect homeowners from the risks. The series of fires, which started last week and are still raging, are the most destructive in LA County history, destroying at least 12,300 structures so far and killing 24 people. Left in the lurch are homeowners in particularly disaster-prone areas like Chandler, who lack the insurance protection that eases the process of navigating such profound grief.

An insurance crisis

In April 2024, State Farm, one of the largest insurers in California, canceled hundreds of policies in Pacific Palisades, causing roughly 1,600 insured homes in the area to lose coverage. In recent years, the company and other private insurers have been progressively scaling back coverage in the areas most prone to wildfire disasters. According to a tally by the San Francisco Chronicle, Pacific Palisades experienced 1,930 policy nonrenewals between 2019 and 2024. Insurance companies cite the growing riskiness of offering insurance in places so vulnerable to catastrophic weather events, particularly given state regulations that bar companies from raising rates to a level that might adequately reflect that risk.

In light of the departures of major private insurers, California policymakers have begun to make legislative attempts at both mitigating the harm of recent policy cancellations and luring insurers back to these more vulnerable areas of the state. In 2018, California Insurance Commissioner Ricardo Lara established a one-year moratorium on policy cancellations for areas that have been struck by wildfires. A running list of eligible ZIP codes under the policy is maintained by the commissioner’s office.

Kenneth Klein, professor of law at California Western School of Law, said that while the moratorium is better than nothing, it would be notably more effective if it was extended to a year after the owners have reoccupied their damaged home.

“It’s worth recognizing that the vast majority of people who have had their homes destroyed in this fire will not be back in their homes within one year, and so the math tells us [the moratorium] is unlikely to impact most homeowners,” said Klein, whose expertise includes firsthand experience: In 2003, Klein lost his own home in the San Diego Cedar Fire.

Meanwhile, in December 2024, the state issued a new regulation mandating that insurance companies offer coverage to residents in at-risk areas by requiring that insurers write policies in areas “equivalent to no less than 85 percent of their statewide market share.” The 85% threshold, however, will not immediately be enforced. Rather, insurers will have to match a 5% increase every two years.

As private insurers flee, individual California homeowners have increasingly turned to the FAIR Plan, insurance offered through the state that is often considered to be a “last resort.” Almost half a million Californians have insurance under the FAIR Plan.

Unsurprisingly, FAIR Plan sign-ups have increased most in counties with higher wildfire risks. According to reporting from Bloomberg, Pacific Palisades is the state’s fifth-largest user of FAIR policies, collectively accounting for almost $6 billion in exposure.

Klein said the most effective insurance should satisfy three criteria: affordability, availability, and adequacy. While FAIR is available for all within the state, he said it’s not the most ideal, long-term option across the board.

FAIR also helps prospective homeowners whose mortgage plans require home insurance when they’ve been denied by private insurers.

“That is not trivial. A home is a critical piece of building generational wealth,” Klein said. “But [while] insurance under the FAIR Plan will satisfy your mortgage lender, it is often less robust coverage than you would get in the private markets. It’s a solution, but it’s often not a great solution.”

While the insurance crisis in California has been in the spotlight, these issues are also plaguing other regions across the country, such as Florida, a state that is also uniquely susceptible to climate disasters.

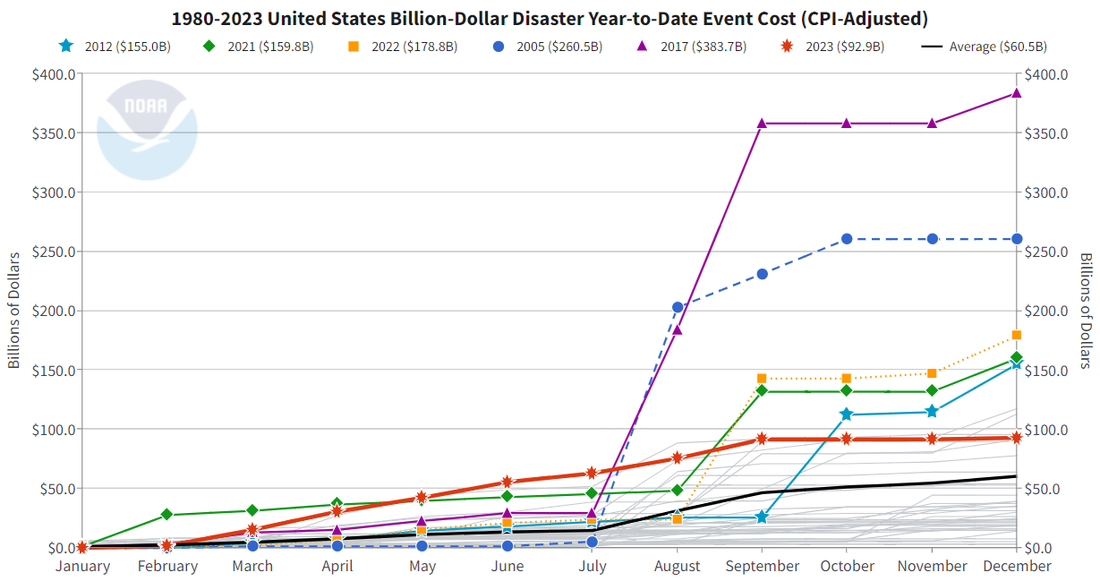

According to data from the National Centers for Environmental Information, between 2019 and 2023, Florida experienced 24 disaster events that cost more than $1 billion each. The total costs associated with those catastrophes hover around $240 billion. In the aftermath of two hurricanes in 2022, insurance rates across the state have quadrupled the national average. Throughout the state, private insurers have also canceled policies, leading more than 1 million Florida residents to join the state-operated insurance system Citizens Property Insurance Corporation.

Inclusive insurance

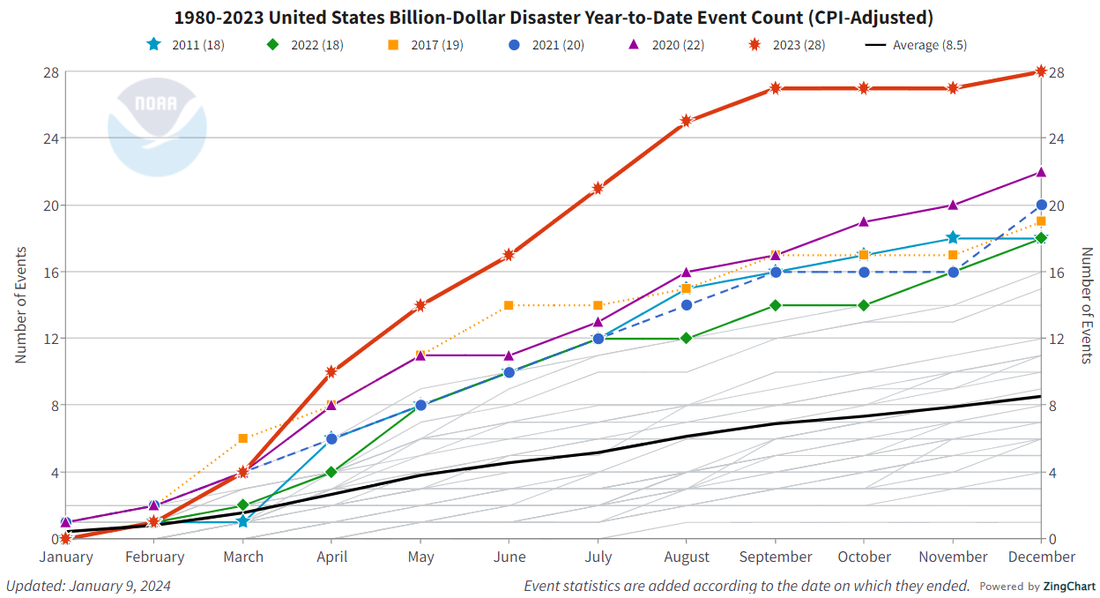

Climate change is forcing policymakers across the country to rethink insurance models, particularly as areas formerly excluded from conversations about natural disasters begin to face their own severe weather events. According to federal data, 28 separate natural disasters in the U.S. caused at least $1 billion each in damage in 2023. In the last five years, there have been 102 disaster events, a steep increase from 57 in the 1990s and 33 in the 1980s.

Just as states and cities are growing increasingly ill-equipped to manage the scope and frequency of these events, so, too, are individual homeowners who are becoming vulnerable in ways they may not even fully realize. In his research, Klein has found that almost 80% of American homeowners do not have adequate coverage. A survey conducted by Bankrate shows that 26% of U.S. homeowners report being unprepared for the potential costs related to severe weather events.

While attention has primarily been paid to areas like Pacific Palisades, the places that will take the longest to rebuild are communities that are traditionally underinsured or uninsured compared to the national average. In response, researchers like Carolyn Kousky, founder of the nonprofit Insurance for Good, have proposed strategies toward “inclusive insurance” models that make insurance coverage more accessible to those locked out of the market. Among the proposals brought forth are “microinsurance” or low-coverage, low-premium insurance options that are subsidized by various entities such as the public sector, philanthropies, or even nonprofit organizations.

Meanwhile, according to Klein, interventions made in the health care insurance sector, namely the Affordable Care Act, could serve as a potential model for home insurance reforms. Klein said that features such as community pricing have been effective for health insurance and can have parallels for homeowners. This could require companies to write home insurance policies across the entire state and view the whole state as a single insurance pool for evaluating risk for certain severe events, such as fire.

“Then what you would see is people who lived in low fire-rate spaces, which is the majority of the state, would see their insurance go up a little bit. The rest of the state would see their insurance go down a lot, and everybody would have—at least in theory, just like the Affordable Care Act, regardless of their risk profile—access to insurance.”

Preserving Altadena and rebuilding lives

Of particularly high concern are overwhelmingly underinsured neighborhoods like Altadena, Klein said, where homes have been passed down generationally. Inherited homes that have long been paid off and thus, no longer require insurance coverage often tend to be the only or one of few family assets and a key source of generational wealth. Their loss can be particularly devastating.

“The only way that I could envision Altadena preserving its diversity would be to have reconstruction subsidies funded by private philanthropies, the government, or a private-public partnership that conditioned that when the home was completed, it would carry insurance,” said Klein.

Klein, among other observers and experts, pointed to parallels between Altadena and areas like New Orleans’ Ninth Ward. Much like Altadena, the Ninth Ward was notable for the prevalence of multi-generationally owned homes and the low insurance protection that often accompanies them. In the almost 20 years since Hurricane Katrina, the region has struggled to fully rebuild.

Chandler’s family has called Altadena, a community in the San Gabriel Valley, home since they moved to the neighborhood in the 1970s. Despite its rich Black history, Altadena has been rapidly growing wealthier and whiter over the past decade, Chandler and his wife Monica Brown said. As the area gentrifies, offers have come in seeking to displace Black families with multigenerational roots. Chandler said that as soon as his grandfather passed away, he began receiving cash offers in the mail. Now, Brown said, more predatory investors are reaching out, asking to purchase the land on which their prized home recently stood.

“I just pray somehow we could raise enough money so that this doesn’t have to happen and that these Black and brown families don’t feel like we have to sell our land in order to survive,” Brown said. She urged others in the neighborhood to lean on one another and not sell to big investors. “Even if you feel like you need to sell, join our community, and we can try to find somebody who actually cares about the history of Altadena to buy it.”

Chandler has attempted to work with his home’s prior insurer, hoping that his family’s longstanding relationship with them might leave room for some grace.

“My grandfather’s been a customer for over 40 years, never missed a payment, never filed a claim, and so currently I’m in the process of [seeing] if they’ll work with me and give me a chance to be reinstated,” Chandler said, adding that he would be willing to pay a penalty and reinstatement fee. “Right now, the thing that’s killing me the most is not knowing if I’m going to be able to rebuild if I don’t get this insurance company to work with me and give me a chance.”

Author

Tamar Sarai is a writer, journalist, and historian in training. Her work focuses on race, culture, and the criminal legal system. She is currently pursing her PhD in History at Temple University where

Sign up for Prism newsletters.

Stay up to date with curated collection of our top stories.